The Price Waterfall in Agriculture Machinery: Where Spare Parts Margin Quietly Disappears

Pass the tariff through, lose share. Absorb it, lose margin. The price waterfall is the third option, and MP ONE makes it operational.

Content:

- What the Price Waterfall Reveals for Agriculture OEMs?

- Where the Margin Is Going?

- How the Waterfall Behaves on One Part?

- What a Working Waterfall Actually Needs?

- What Changes the Day You See It All?

- Stop Watching Margin Walk Out the Door

There are two bad answers to the tariff on every SKU. Raise prices to cover it, and you accelerate the customer shift to will-fitters. Absorb it, and you give back margin you cannot afford to lose, because U.S. ag equipment sales fell sharply through 2025 — AEM reported U.S. tractor sales down 19.6% and combine sales down 35.2% YoY in November 2025 alone (with peak monthly combine drops earlier in the year reaching nearly 50%) — part of a broad decline running through the year — and parts are now carrying your P&L.

The annual pricing cycle gives you no third answer.

The third answer lives inside the price waterfall.

What the Price Waterfall Reveals for Agriculture OEMs?

The price waterfall is the path a part takes from list to pocket. List, dealer discount, regional adjustment, customer rebate, off-invoice items, freight, returns. Each step is small. Each is invisible to the next one upstream. Most agriculture OEMs see two numbers, the top (list) and the bottom (gross margin at year-end). Everything between is dark.

Right now, that dark stretch is under unusual stress:

- Tariffs that move faster than your pricing cycle. U.S. Section 232 steel and aluminium tariffs took effect at 25% on March 12, 2025 (reduced to 15% as of June 8, 2026) and doubled to a 50% effective rate in June 2025, with China's 10% retaliatory tariff on U.S. farm equipment effective February 10, 2025 on top. Input costs move quarterly. Your pricing window is annual.

- A margin engine that has moved to parts. Equipment sales are off sharply. The aftermarket is now where the year is won or lost.

- Will-fitters sharpening their attack. Independent aftermarket suppliers, known as will-fitters because their parts fit OEM equipment without being OEM-built, like A&I Products and KMP Brand, compete hardest on the high-volume SKUs the end customer replaces most often.

- Right-to-repair legislation hardening. in the U.S. and EU, pushing more parts revenue toward independent repair.

Four pressures, one waterfall. The OEMs that hold margin in 2026 are the ones that can actually see it.

Where the Margin Is Going?

You probably recognise at least three of these:

- Cost-plus pricing with no read on the market. You set markup on cost. Will-fitters set price on what the end customer will pay. Two different games. Yours leaves money on critical parts and overshoots on commodity ones. Both your dealer and your customer notice.

- An annual review in a quarterly market. Tariffs moved in March. Then in June. Your next pricing window is January. Margin has been eroding for nine months, and you find out at the year-end review.

- A harvest premium nobody captures. A combine that will not run in late September is not a maintenance question. It is a revenue emergency for the end customer. Demand on the part is inelastic. Most OEMs price September the same way they price February.

- One rebate for every part. A 3% volume rebate paid on a commodity filter and on a downtime-critical hydraulic component. The filter probably needed a different defense entirely. The hydraulic component should never have given anything up.

- A waterfall nobody owns. Corporate sets list. Sales negotiates discount. Finance reconciles off-invoice. Pricing data lives across ERP, DMS, and dealer systems. Nobody watches the whole path at the SKU level, so nobody knows where the leak is. Only that it happened.

This is the part most internal initiatives underestimate. It is not a tooling problem first. It is an accountability problem. Corporate is rewarded for list discipline, sales for volume, finance for off-invoice clean-up. Each function is locally rational. The leak survives because no single role is paid to close it. Any platform that does not also force the conversation across those three teams will be installed, ignored, and quietly worked around inside two cycles.

Want to see what this looks like on your own portfolio?

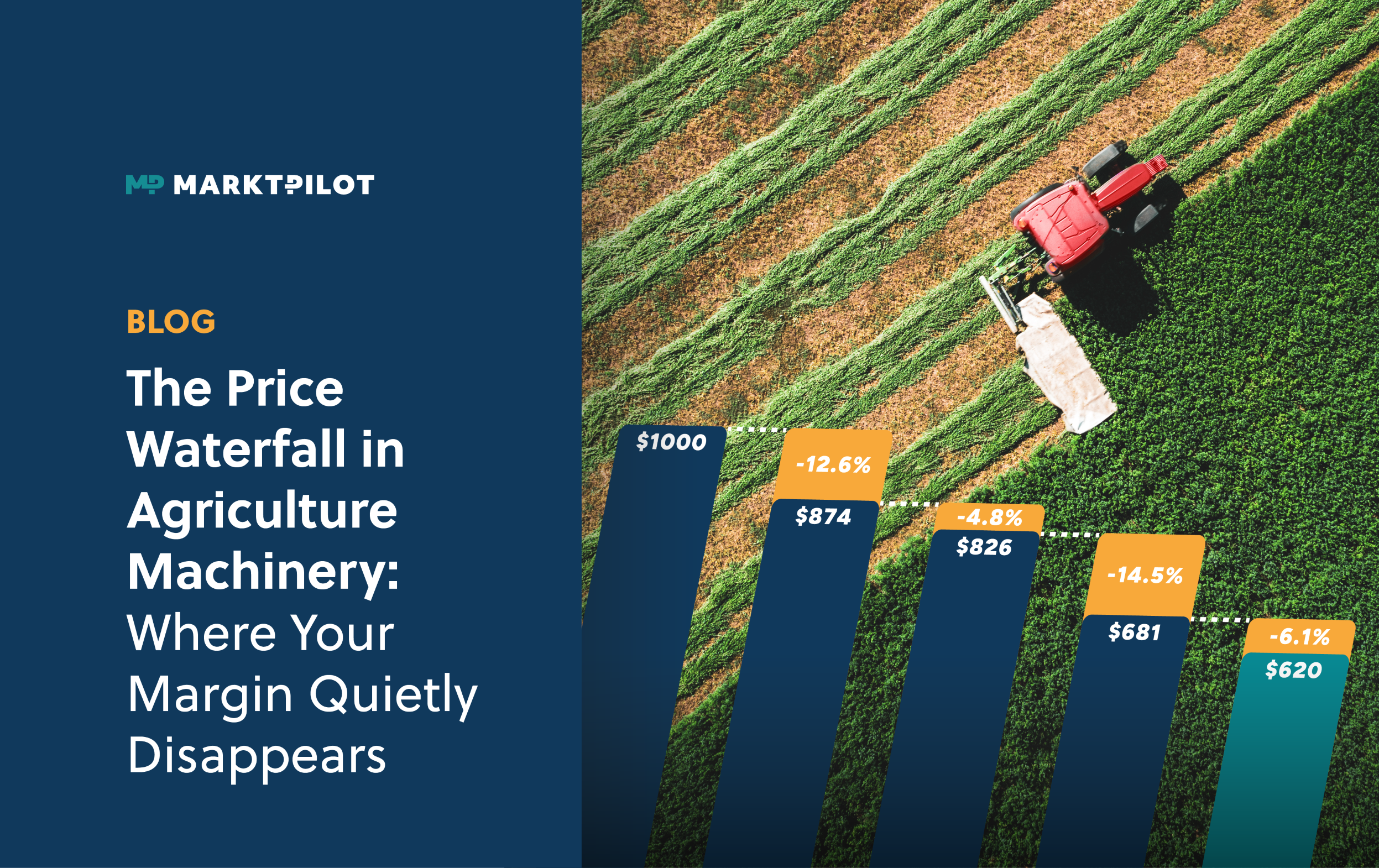

How the Waterfall Behaves on One Part?

A single SKU. A hydraulic cylinder. It ships across virtually every category in the agriculture portfolio: tractors, combines, balers, sprayers, tillage. Will-fit competition on this class of part is heavy. It sells through dealer, distributor, and direct channels. The same pattern shows up on combine headers, hydraulic pumps, and any high-criticality service item where the end customer has no substitute on harvest day.

The list price below is an example value. The structure is what happens in real portfolios every day.

A third of the value disappears between list and pocket. Roughly ten to eleven percentage points of that is recoverable: the flat rebate on a part the customer would not have substituted, the regional adjustment without market data, the off-invoice items nobody tracks at the SKU level.

One percent on this single SKU is USD 12 per unit. Across an active portfolio of 50,000 SKUs sold thousands of times a year, the recoverable margin stops being interesting in dollars and starts being interesting in millions.

What a Working Waterfall Actually Needs?

Whatever you build or buy, three capabilities have to work together. Any one of them in isolation will not move pocket margin.

- Market intelligence at the SKU level, refreshing in days rather than years, with will-fit cross-references included. So you know where the threat actually sits, before the dealer call.

- Pricing logic that knows the difference between a filter and a hydraulic cylinder, and applies different defense to each. With governance for dealer, distributor, and direct channels.

- Net price realisation visible end-to-end, with simulation before you push a change. So a tariff pass-through is tested in a sandbox before it touches the dealer file.

Without those three, pricing is one bad season away from carrying losses the new equipment side cannot offset.

“Equipment sales are off sharply. The aftermarket is now where the year is won or lost.”

What Changes the Day You See It All?

MP ONE™ is one answer to this. Whatever platform you put behind it, the shift in day-to-day pricing work looks the same:

- You stop discovering the leak at the year-end review. You see it the day it opens, on the SKUs where it matters.

- You stop pushing 3% across the board. You pick the SKUs where a tariff pass-through actually holds, and you leave the rest alone.

- You stop dreading the dealer call. You show up with the market data, the cross-references, and the rationale documented before anyone asks.

- You stop wondering whether last year's price update made it to pocket. You watch it land in real time.

- You stop treating a hydraulic cylinder and a filter the same way. Each part defends its own margin on its own terms.

That is the shift. One way to deliver it — and the way MP ONE does — is by unifying three capabilities most agriculture OEMs currently have scattered across systems and teams. The Intelligence Engine watches the market continuously. The Decision Engine applies pricing logic at the SKU and channel level. The Performance Engine tracks what is actually realized in the pocket. One platform, one waterfall, one source of truth.

You can check your price waterfall calculator below.

Stop Watching Margin Walk Out the Door

You do not have another full pricing cycle to figure this out. Will-fitters are not waiting. Tariffs are not pausing. The dealer network is not getting more patient.

Every quarter your competitor runs on a continuous waterfall and you run on an annual one, they take margin you did not know you had.

The agriculture OEMs that come out of this cycle with their margin intact will have done one thing in common: they will have killed the annual pricing review as a primary instrument. It will still happen, but as a sanity check on a process that runs every week. The OEMs that treat 2026 as another January-to-January exercise will spend the second half of the decade explaining to their boards why parts margin kept slipping in a market where they were supposed to own the customer.